The psychology of spending: How your emotions influence your personal budget

The Emotional Connection to Spending

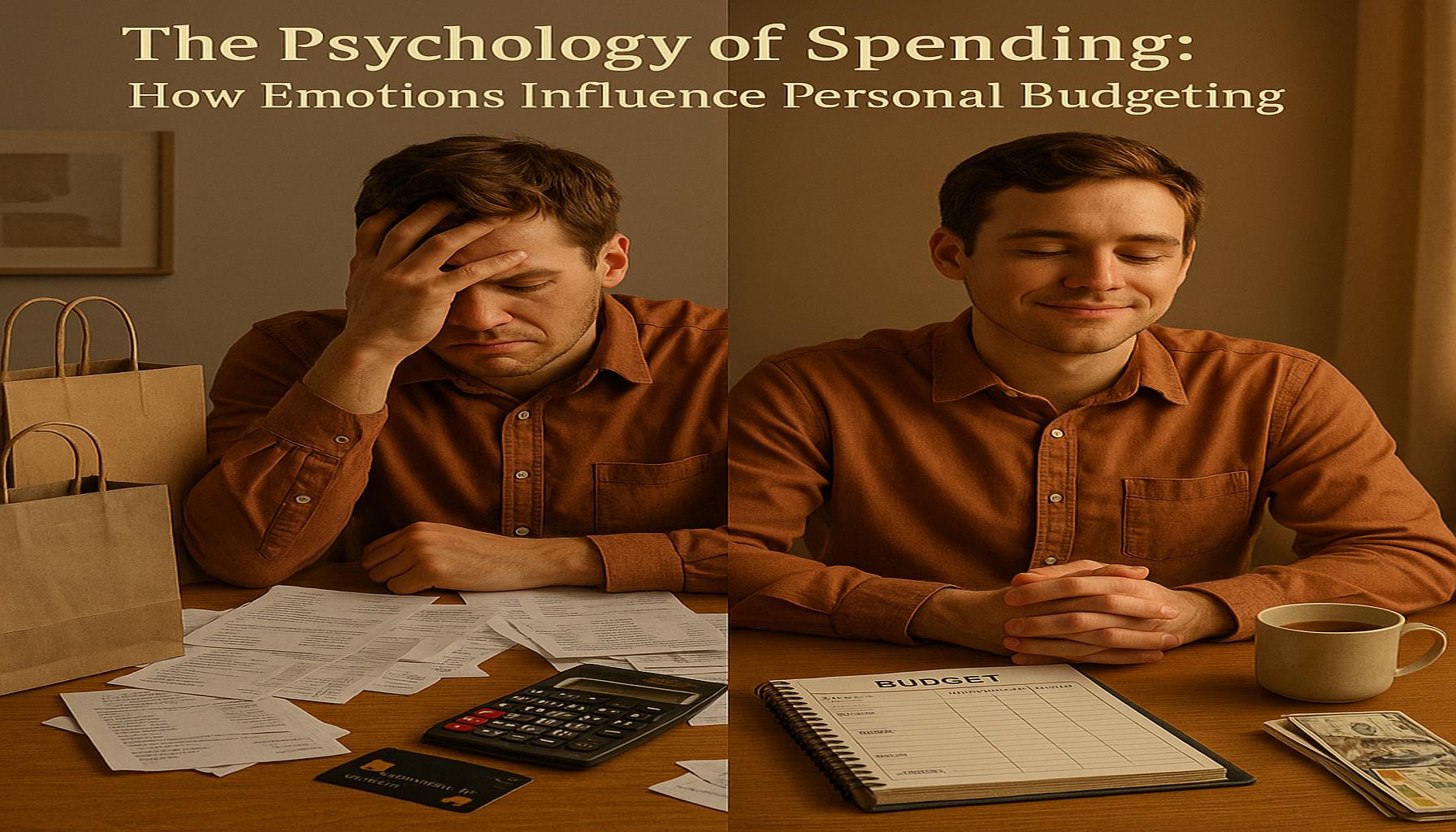

Have you ever found yourself purchasing that trendy outfit or the latest gadget after a long, stressful day? Such behaviors often stem from emotional influences that can significantly affect our spending habits. Understanding this emotional connection is crucial for effective budget management and making informed financial decisions.

Our emotions can profoundly impact how we handle money, leading to both positive and negative shopping behaviors. To better understand these influences, here are some key factors:

- Emotional Triggers: Many individuals experience emotional states such as stress, happiness, or even boredom, which greatly influence their spending behaviors. For example, you might splurge on a night out after a stressful work week as a way to alleviate your feelings. Alternatively, when feeling low, you may turn to shopping for comfort, leading to impulse purchases that you might later regret.

- Retail Therapy: The concept of retail therapy refers to the act of shopping to improve one’s mood. While it can provide momentary joy, it often results in overspending. According to a study, a significant percentage of consumers in the UK have admitted to making impulse buys in an attempt to boost their spirits. This short-lived happiness can spiral into financial stress when the reality of those expenditures hits home.

- Social Influence: The pressure to keep up with peers can drive individuals to make purchases beyond their means. For instance, seeing friends wearing the latest styles or driving flashy cars may prompt you to invest in expensive items to feel accepted or valued. Such decisions, driven by social comparisons, can contribute to a cycle of debt and anxiety.

Recognising these emotional influences is essential for maintaining a healthy budget. By understanding your emotional triggers, you can make more informed financial decisions. For example, if you identify that shopping during stressful periods leads to overspending, it may be wise to seek healthier coping strategies, such as engaging in exercise or socialising with friends instead.

In the following sections, we will explore practical ways to identify these emotional triggers and develop strategies to manage spending sustainably. With this knowledge, you can create a budget that not only reflects your financial goals but also prioritises your emotional well-being. By engaging with both your emotions and finances, you can work towards a more balanced and fulfilling life.

DISCOVER MORE: Click here for a seamless guide

Understanding Emotional Spending Patterns

Emotional spending often operates on a subconscious level, leading individuals to make purchases that align with their current emotional states. To effectively manage your finances, it’s essential to become aware of these emotional patterns. By examining how specific feelings influence your purchasing decisions, you can develop strategies to mitigate unnecessary spending. Let’s take a closer look at the common emotional spending patterns and how they manifest in our daily lives:

- Stress Purchases: Many people find themselves shopping as a way to cope with stress. After a particularly demanding day at work, for instance, you may venture into a local shop to seek comfort in new purchases. While this might provide temporary relief, it can quickly lead to an accumulation of items that don’t necessarily add value to your life, creating additional financial strain.

- Celebratory Spending: Celebrating milestones and achievements often leads to considered purchases intended to treat oneself. However, it’s crucial to ensure that these celebrations don’t compromise your budget. For example, treating yourself to a fancy dinner or a short getaway can be enjoyable but should align with your financial goals. Planning such expenditures in advance can keep you within budget while still allowing you to indulge.

- Boredom Shopping: Feeling bored or restless can trigger the desire to shop, often leading to impulsive purchases. This behavior may stem from wanting to fill a void or seeking stimulation. Engaging in activities that promote creativity or learning, rather than heading to the shops, can help redirect these feelings toward more fulfilling experiences.

- Comparison Spending: In our social media-driven world, the tendency to compare ourselves to others can fuel unhealthy spending habits. Scrolling through posts showcasing extravagant lifestyles, luxurious vacations, or the latest fashion can result in feelings of inadequacy, prompting you to overspend in an attempt to keep up. Recognising that everyone’s financial situation is unique can help alleviate this pressure.

By identifying these emotional spending patterns, you can begin to take charge of your finances. Start by keeping a spending diary where you track not only your purchases but also the emotions you experienced at the time. Over time, these records can reveal trends and help you build a clearer understanding of how your feelings influence your spending decisions.

Additionally, consider implementing mindful spending practices that encourage reflection before making a purchase. Ask yourself whether the item truly aligns with your values and budget, or if you are acting on impulse driven by emotion. Greater awareness and intentionality in your spending can lead to better financial outcomes and a healthier relationship with money.

CHECK THIS OUT: Click here to get your credit card easily

The Consequences of Emotional Spending

While understanding emotional spending patterns is crucial, it’s equally important to recognize the potential consequences that may arise from this behaviour. Acknowledging these impacts can empower you to change your spending habits and improve your overall financial well-being. Below are some significant consequences associated with emotional spending:

- Debt Accumulation: Engaging in emotional spending can lead to overspending, resulting in increased credit card debt or loans. When individuals rely on credit to make purchases as a way to manage emotions, they often find themselves in a cycle of borrowing that can be difficult to escape. It’s vital to remember that what might feel like a small comfort in the moment could lead to larger financial burdens in the long run.

- Regret and Guilt: Post-purchase regret is a common experience for those who buy on impulse based on their emotions. After the thrill of the purchase wears off, one can feel guilty or disappointed, especially if the item doesn’t provide the expected satisfaction. This guilt can compound emotional distress, leading to further poor financial decisions. Developing an awareness of your emotional triggers and the aftermath of impulsive spending can help mitigate these feelings.

- Impact on Relationships: Financial stress stemming from emotional spending can strain relationships with family and friends. Disagreements over money matters, especially if one partner tends to overspend, can lead to tension and resentment. Communication about financial goals and spending habits is vital for maintaining healthy relationships, so consider having open discussions about your expenditures and how they align with your shared goals.

- Lower Financial Stability: Relying on emotional spending as a coping mechanism can hinder your capacity to build savings, invest for future goals, or prepare for unexpected circumstances. A lack of financial stability can create anxiety, which may keep you in a cycle of emotional spending. Prioritising budgeting and creating a financial plan can help establish a stronger foundation and increase your sense of control over your finances.

To combat the negative repercussions of emotional spending, consider implementing a few strategies that foster a more disciplined approach to your finances. One effective method is the use of spending limits. Establish a set amount of money you can allocate for discretionary spending each month. Once you’ve reached that limit, commit to refraining from additional purchases; this can help develop self-control and curb emotional impulses.

Another strategy is to create a ‘cooling-off’ period for larger purchases. If you’re tempted to buy something that you think will satisfy an emotional need, wait at least 24 hours before making a decision. This gives you time to reflect on whether the item genuinely aligns with your financial objectives or if the desire was simply a fleeting emotional response.

Engaging in alternative coping mechanisms can also be beneficial. Instead of turning to shopping during moments of emotional instability, consider healthier outlets such as exercise, meditation, or pursuing new hobbies. This shift in behaviour not only helps alleviate emotional distress but can also save you money in the process.

Ultimately, cultivating an understanding of the psychology behind your spending allows you to take proactive steps toward healthier financial practices. By recognising the influences of emotion on your purchasing decisions, you can develop effective methods to align your spending with your financial goals.

DIVE DEEPER: Click here to discover investment strategies</

Conclusion

Understanding the interplay between emotions and spending habits is essential in creating a stable financial future. Throughout this article, we have explored how emotional triggers can lead to impulsive purchasing decisions, often resulting in debt, regret, and strain on relationships. By recognising these patterns, you empower yourself to take control of your finances and ensure that your spending aligns with your long-term goals rather than your immediate feelings.

It is evident that adopting practical strategies, such as setting spending limits and implementing a ‘cooling-off’ period before making larger purchases, can significantly contribute to healthier financial decisions. Additionally, cultivating alternative coping mechanisms like engaging in physical activities or creative hobbies can replace the instinct to shop during moments of emotional vulnerability. These approaches not only help you manage your emotions more effectively but also safeguard your financial well-being.

Ultimately, being mindful of the psychological factors influencing your spending will lead to greater awareness and improved financial literacy. By taking charge of your emotional spending, you can transform your relationship with money, contributing to both your emotional well-being and financial stability. Remember, the goal isn’t to eliminate spending altogether, but rather to ensure that your financial choices resonate with your true values and aspirations.

Related posts:

How to Create an Effective Personal Budget: Practical Tips for Daily Life

Financial Planning Techniques for Couples: How to Combine Budgets Without Conflict

How Inflation Affects Your Personal Budget and Strategies to Protect Yourself

How to Use Personal Finance Apps to Optimize Your Budget

The role of financial education in building a sustainable and realistic budget

The impact of financial goals on the motivation to maintain a personal budget

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.