How to Create an Effective Personal Budget: Practical Tips for Daily Life

Understanding the Importance of Budgeting

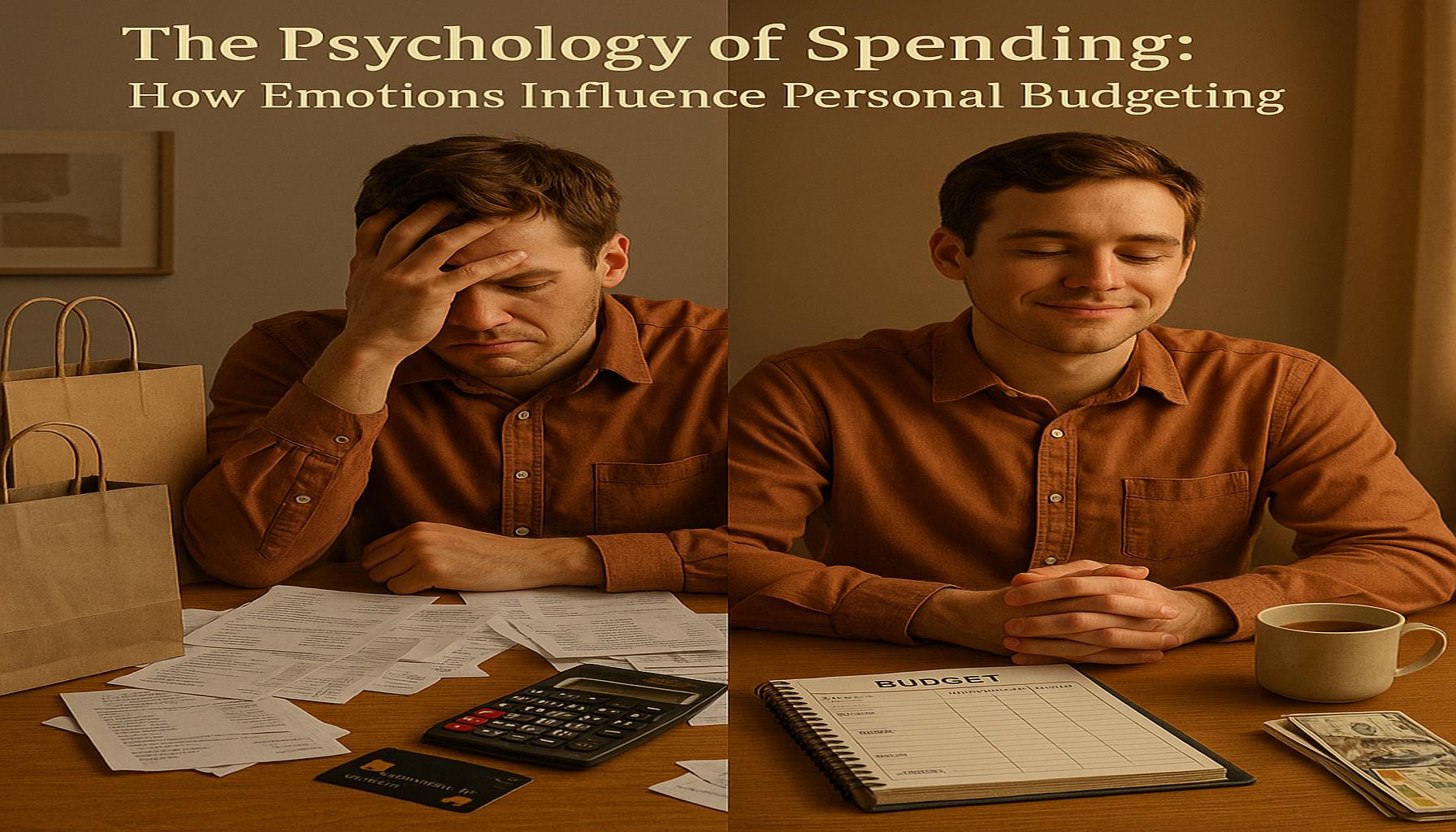

Creating a personal budget is essential for maintaining financial health. A well-structured budget allows you to track your income and expenses, ultimately helping you to achieve your financial goals. By knowing exactly where your money is going, you gain not only a sense of control but also a clearer path to financial stability.

Why is budgeting important? Here are a few key benefits that illustrate the purpose and advantages of maintaining a budget:

- Control Over Finances: A budget provides you with a clear understanding of where your money goes. For instance, if you regularly find yourself low on funds at the end of the month, a budget can help you pinpoint whether you’re spending excessively on takeaways or subscriptions.

- Identify Spending Habits: Tracking your expenses allows you to identify patterns in your spending. Perhaps you discover that you frequently spend more on coffee than you anticipated. By recognizing this, you can make informed decisions, like brewing coffee at home, thereby saving money.

- Save for the Future: A solid budget helps in setting aside funds for emergencies, holidays, or major purchases. Whether you need to save for that dream holiday to the Greek islands or build an emergency fund to cover unexpected expenses like car repairs, budgeting makes it achievable.

One of the most encouraging aspects of budgeting is that it can be straightforward and manageable. The process doesn’t have to be daunting. By following some simple steps, you can tailor a budget that suits your lifestyle and financial needs. Start by listing all your sources of income and all your necessary expenses, such as rent, utilities, groceries, and transportation costs.

In this article, we will cover:

- Key components of an effective budget

- Practical tips for daily budgeting that you can incorporate into your routine

- Tools and resources that can help you stay on track, including popular budgeting apps available in the UK

With patience and a little bit of effort, you’ll be able to take control of your finances and make confident spending choices. Providing consistent attention to your budget will empower you to reach your financial goals and improve your overall financial well-being. Let’s get started on your journey to financial stability!

DISCOVER MORE: Click here for a step-by-step guide

Key Components of an Effective Budget

To create a personal budget that works for you, it’s vital to understand its key components. A budget generally consists of two main segments: income and expenses. By clearly defining these elements, you can create a solid foundation that helps you gain control over your finances. Let’s break down each of these components in more detail:

1. Identifying Your Income

The first step in budgeting is to accurately identify your income. This includes not just your salary but any additional sources of income you may have. For instance, if you receive rental income, freelance payments, or even benefits like Child Benefit or Universal Credit, this should all be included. List these down to understand the total amount you have coming in each month.

2. Categorizing Your Expenses

Once you have a clear picture of your income, the next step is identifying and categorizing your expenses. It’s crucial to distinguish between fixed and variable expenses:

- Fixed Expenses: These are costs that remain constant from month to month, such as rent or mortgage payments, utility bills, and subscriptions. For example, if your rent is £750 a month and your utilities typically amount to £100, you can calculate these fixed costs easily.

- Variable Expenses: These are costs that can fluctuate each month, such as groceries, entertainment, and dining out. To budget for these, look at your spending habits over the past few months. If you usually spend around £250 on groceries and £100 on takeaways, note these as your variable expenses.

3. Setting Financial Goals

Another critical aspect of budgeting is establishing financial goals. Understanding what you want to achieve with your budget—whether it’s saving for a holiday, building an emergency fund, or paying off debt—will guide your spending decisions. Try to set specific, measurable goals. For example, “I want to save £1,000 for a holiday within the next six months” is clearer and more achievable than simply stating, “I want to save money.”

4. Tracking and Reviewing Your Budget Regularly

Creating your budget is just the beginning; it’s essential to track your spending and review your budget regularly. Set aside time each week or month to assess your spending against your budget. This will allow you to see where you might be going overboard and make necessary adjustments. Use simple spreadsheets or budgeting apps to help keep your budget in check and easy to review.

Remember, the key to a successful budget lies in its adaptability. Life circumstances change, and so will your financial situation. Having a flexible budget will help you accommodate unexpected expenses or shifts in income.

The next section will provide you with practical tips for daily budgeting that can be seamlessly incorporated into your routine, helping you adhere to your financial goals while enjoying daily life.

LEARN MORE: Click here to discover how to apply

Practical Tips for Daily Budgeting

Now that you have a solid foundation for your personal budget, it’s time to delve into practical tips that you can apply in your daily life. Proper budgeting isn’t just about setting targets; it’s about integrating money management habits into your routine. Here are some actionable strategies that can help you remain on track with your financial goals:

1. Use the 50/30/20 Rule

This widely recognized budgeting method can simplify your money management efforts. Allocate your after-tax income into three categories: 50% for needs (essential expenses such as housing, groceries, and utilities), 30% for wants (non-essential spending like dining out and entertainment), and 20% for savings or debt repayment. For instance, if your monthly income is £2,000, you would aim to spend no more than £1,000 on needs, £600 on wants, and £400 on savings or debt repayment. This structured approach helps ensure that you’re not overspending in any area.

2. Implement Cash Envelopes for Discretionary Spending

If you find it challenging to control your discretionary spending, consider the cash envelope system. Withdraw your budget for categories like groceries or dining out in cash and place it into designated envelopes. When the cash is gone, it signifies you’ve exhausted your budget for that category. This tangible method often prevents impulse purchases and helps enforce discipline when spending.

3. Regularly Use Budgeting Apps or Tools

Modern technology offers numerous apps and tools designed to assist with budgeting. Platforms like Mint, YNAB (You Need A Budget), or even simple spreadsheets can track your income and expenses, allowing for easy adjustments. These tools provide valuable insights into your spending habits, helping you stay accountable and informed on your financial journey.

4. Adjust Your Budget According to Seasons

Your spending might change with the seasons—for example, heating bills may rise in winter or holiday shopping may spike in December. Review your budget regularly to account for these variances. If you anticipate spending more in a particular month, such as for holidays, adjust your budget accordingly by saving a little extra in the previous months to alleviate any financial stress. This proactive approach helps mitigate potential financial strain.

5. Prioritise Your Savings with Automatic Transfers

One of the best ways to ensure you save money consistently is to set up automatic transfers from your current account to your savings account. Treat your savings like a non-negotiable expense by allocating funds right after your income is deposited. For example, if you aim to save £100 each month, ask your bank to transfer that amount as soon as your wages are paid. This way, saving becomes an automatic part of your financial routine, reducing the temptation to spend that money.

6. Hold Monthly Finance Meetings

If you’re budgeting as a household or with a partner, regular finance meetings can foster transparency and communication surrounding your finances. Set aside time each month to discuss your budget, review progress toward financial goals, and make adjustments where necessary. This collaboration ensures everyone involved is aligned and aware of the financial priorities, reinforcing shared responsibility.

Incorporating these practical budgeting techniques into your everyday life can transform your financial management from a daunting task to a manageable routine. By making small, consistent changes, you can cultivate a healthier relationship with your finances, ultimately helping you reach your long-term financial goals.

DISCOVER MORE: Click here to find out how to apply

Conclusion

Creating an effective personal budget is more than just tracking expenses; it’s about fostering a disciplined approach to your financial life. By implementing practical tips and techniques, you can take control of your finances and build a secure future. Remember the critical components: define your income, categorise your expenses, and set realistic savings goals. The 50/30/20 rule, for instance, serves as a helpful guide to distribute your funds wisely, while tools like cash envelopes and budgeting apps can help reinforce your plans.

Adjustments to your budget are essential, especially with seasonal changes or unexpected financial events. Being proactive and adapting your strategies prepares you for eventualities that could disrupt your financial goals. By prioritising savings through methods such as automatic transfers, you embed a habit that pays dividends in the long run. Moreover, if you share financial responsibilities with a partner or family, monthly finance meetings can foster transparency and ensure everyone is working towards shared objectives.

Ultimately, budgeting should be a dynamic process, reflecting your evolving needs and goals. As you embark on this journey, remember that small, consistent changes can lead to a significant impact. With discipline and careful planning, you’ll not only improve your financial situation but also gain peace of mind, enabling you to focus on what truly matters in life. Embrace budgeting as a valuable skill that empowers you to make informed choices and achieve your financial aspirations.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.